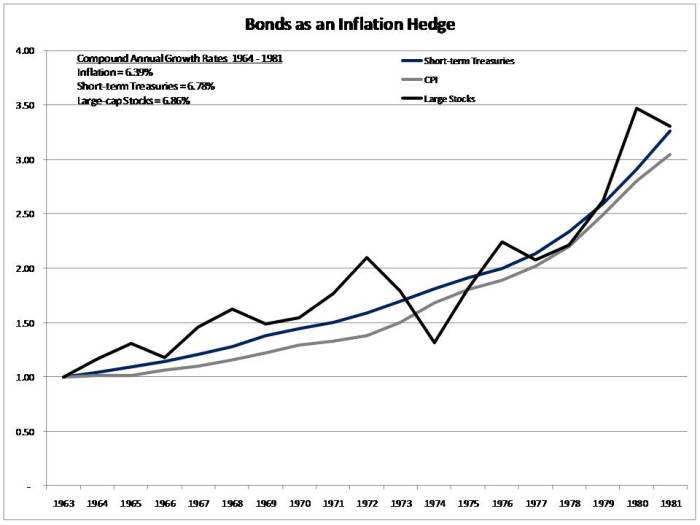

What is an Inflation Hedge? sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with casual formal language style and brimming with originality from the outset.

Inflation hedge is a crucial concept in the financial realm, providing protection against the eroding effects of inflation on investments. Let’s delve into the specifics of this key strategy and explore its significance in building a robust investment portfolio.

Explaining Inflation Hedge

In the realm of finance, an inflation hedge refers to an investment or asset that tends to retain or increase its value over time, acting as a safeguard against the erosive effects of inflation on purchasing power.An inflation hedge is crucial for investors looking to protect their wealth and maintain the real value of their assets in times of rising prices.

By including inflation hedges in their portfolios, investors aim to counter the negative impact of inflation on the returns of their investments.

Assets commonly used as Inflation Hedges

- Real Estate: Properties and real estate investments often appreciate in value over time, providing a hedge against inflation.

- Gold and Precious Metals: These commodities have a long history of retaining value during inflationary periods.

- TIPS (Treasury Inflation-Protected Securities): These bonds are indexed to inflation, ensuring that the principal and interest payments adjust with changes in the Consumer Price Index.

- Commodities: Assets such as oil, agricultural products, and industrial metals can serve as inflation hedges due to their tangible nature and demand.

Income Funds

Income funds are a type of mutual fund that focuses on generating regular income for investors through dividends, interest payments, and other distributions. These funds are popular among investors seeking a steady stream of income while also benefiting from potential capital appreciation.

Differentiate between income funds and other types of mutual funds

Income funds are distinct from other types of mutual funds such as growth funds or balanced funds. While growth funds aim for capital appreciation by investing in companies with high growth potential, income funds prioritize generating income through investments in dividend-paying stocks, bonds, and other income-generating securities.

Explain how income funds generate returns for investors

Income funds generate returns for investors primarily through regular distributions in the form of dividends and interest payments. These funds typically hold a diversified portfolio of income-generating assets, which helps in maintaining a consistent stream of income for investors. Additionally, any capital appreciation from the underlying securities can also contribute to the overall returns.

Discuss the risk factors associated with investing in income funds

Investing in income funds comes with certain risk factors that investors should consider. One of the main risks is the interest rate risk, as changes in interest rates can impact the value of fixed-income securities held by the fund. Credit risk is another factor to watch out for, as the default risk of bond issuers can affect the fund’s performance.

Additionally, economic and market conditions can also influence the returns of income funds, making them susceptible to fluctuations in the financial markets.

Index Funds

Index funds are a type of mutual fund or exchange-traded fund (ETF) that aims to replicate the performance of a specific market index, such as the S&P 500. Unlike actively managed funds, which involve a team of professionals making investment decisions to outperform the market, index funds simply aim to match the returns of the index they are tracking.Investing in index funds offers several benefits to investors.

One of the key advantages is their low cost compared to actively managed funds. Since index funds passively track an index, they require less management and research, resulting in lower fees for investors. Additionally, index funds provide diversification across a wide range of securities within the index, reducing individual stock risk.

Comparing Index Funds to Other Investment Options

- Cost: Index funds generally have lower expense ratios compared to actively managed funds, making them a cost-effective investment option for long-term investors.

- Performance: While index funds may not outperform the market, they offer consistent returns that closely mirror the performance of the underlying index. Actively managed funds may have the potential for higher returns but often come with higher fees and the risk of underperformance.

- Diversification: Index funds provide broad exposure to an entire market or specific sector, reducing the risk associated with individual stock selection. This diversification can help investors mitigate risk and achieve more stable returns over time.

Insurance Premiums

Insurance premiums are the amount of money an individual or business pays to an insurance company in exchange for coverage against specified risks. These premiums are typically paid on a regular basis, such as monthly or annually, to maintain the insurance policy.

Calculation of Insurance Premiums

Insurance companies calculate premiums based on a variety of factors, including:

- The type of insurance coverage being purchased

- The amount of coverage required

- The individual’s or business’s level of risk

- The individual’s or business’s claims history

- The location of the insured property

Factors Impacting Insurance Premiums

Several factors can impact insurance premiums, such as:

- Age and gender of the insured individual

- Health status (for health insurance)

- Driving record (for auto insurance)

- Claims history

- Location

Importance of Timely Premium Payments

It is crucial to pay insurance premiums on time to ensure that coverage remains in effect. Failure to pay premiums can result in a lapse in coverage, leaving individuals or businesses vulnerable to financial losses in the event of an unforeseen incident.

In conclusion, understanding what an inflation hedge is and how it can safeguard your investments is essential in today’s economic landscape. By incorporating this strategy into your financial planning, you can better navigate uncertainties and preserve the value of your assets over time.

Questions and Answers

What are the best assets to use as inflation hedges?

Assets like real estate, commodities, and Treasury Inflation-Protected Securities (TIPS) are commonly used as inflation hedges due to their ability to retain value during inflationary periods.

How does an inflation hedge differ from other investment strategies?

An inflation hedge specifically aims to protect investments from the negative impacts of inflation by adjusting their value in response to rising prices, unlike traditional investments that may not account for inflation.

Is it necessary to have an inflation hedge in an investment portfolio?

Having an inflation hedge is crucial to preserve the purchasing power of your investments over time and mitigate the effects of inflation on your overall portfolio returns.