Embark on a journey through the realm of life insurance premiums for 2024, delving into top companies and emerging trends that shape the landscape of this vital financial decision.

Uncover the intricacies of different types of premiums and how individuals can navigate through the sea of options to secure the best coverage for their needs.

Understanding Life Insurance Premiums

Life insurance premiums are the regular payments made by the policyholder to the insurance company in exchange for coverage. These premiums ensure that the policyholder’s beneficiaries will receive a death benefit when the policyholder passes away.

Calculation of Life Insurance Premiums

The calculation of life insurance premiums is based on several factors, including the policyholder’s age, gender, health condition, lifestyle choices, occupation, and the coverage amount desired. Insurance companies also consider the type of policy, such as term life or whole life insurance, and the length of the coverage term.

- Age: Younger individuals typically pay lower premiums as they are considered lower risk compared to older individuals.

- Health Condition: Policyholders in good health are likely to pay lower premiums than those with pre-existing medical conditions.

- Lifestyle Choices: Factors like smoking, excessive drinking, and risky activities can lead to higher premiums.

- Occupation: Some occupations are considered riskier than others, affecting the premium amount.

- Coverage Amount: Higher coverage amounts result in higher premiums.

- Type of Policy: Term life insurance premiums are generally lower than whole life insurance premiums.

Factors Influencing Life Insurance Premiums

Various factors can influence life insurance premiums, including mortality rates, interest rates, inflation, and the insurance company’s expenses and profits.

- Mortality Rates: Insurance companies assess mortality rates to determine the likelihood of a policyholder passing away during the coverage term.

- Interest Rates: The interest rates affect the investment returns of the insurance company, which can impact premium amounts.

- Inflation: Inflation can erode the value of the policy’s benefits over time, leading to adjustments in premium rates.

- Expenses and Profits: Insurance companies factor in their operational expenses and desired profit margins when setting premium rates.

Types of Life Insurance Premiums

Term life insurance premiums are payments made by the policyholder to the insurance company in exchange for coverage for a specific period, typically ranging from 10 to 30 years. These premiums are usually lower compared to other types of life insurance because they only provide coverage for a set term and do not include a cash value component.Whole life insurance premiums, on the other hand, are payments made by the policyholder throughout their lifetime.

These premiums are higher than term life insurance premiums but provide coverage for the insured’s entire life. Whole life insurance also includes a cash value component that grows over time and can be accessed by the policyholder.

Universal Life Insurance Premiums

Universal life insurance premiums are flexible payments that allow the policyholder to adjust the amount and timing of their payments. These premiums consist of two parts: the cost of insurance and the cash value component. The cost of insurance covers the mortality risk, while the cash value component earns interest based on current market rates.

- Universal life insurance premiums offer the flexibility to increase or decrease the death benefit and premium payments.

- The cash value component in universal life insurance allows for potential growth over time, depending on market performance.

- Policyholders can use the cash value to pay premiums or take out loans against the policy.

Best Life Insurance Premiums for 2024

When looking for the best life insurance premiums in 2024, it’s essential to consider various factors such as coverage options, financial stability of the insurance company, and customer reviews. To help you navigate through the sea of options, we have compiled a list of the top insurance companies offering competitive premiums and trends in life insurance premiums for the year 2024.

Top Insurance Companies Offering Competitive Premiums

Below are some of the top insurance companies known for providing competitive premiums in 2024:

- XYZ Insurance Company: XYZ Insurance Company has been consistently offering affordable premiums with comprehensive coverage options.

- ABC Insurance Co: ABC Insurance Co is renowned for its competitive rates and excellent customer service.

- 123 Life Insurance: 123 Life Insurance stands out for its customizable premium options tailored to individual needs.

Trends in Life Insurance Premiums for 2024

For the year 2024, the following trends have been observed in life insurance premiums:

- Overall, premiums have remained relatively stable compared to previous years.

- There is a growing trend towards usage-based insurance, where premiums are determined based on individual behavior and lifestyle choices.

- Some insurance companies are offering discounts on premiums for policyholders who maintain a healthy lifestyle.

How to Find the Best Life Insurance Premiums for Your Needs

Here are some insights on how individuals can find the best life insurance premiums tailored to their needs:

- Compare quotes from multiple insurance companies to find the most competitive premiums.

- Consider the coverage options and policy features offered by each insurance company to ensure they meet your specific needs.

- Look for discounts or incentives that can help lower your premiums, such as bundling policies or maintaining a healthy lifestyle.

Income Funds

Income funds are investment funds that primarily focus on generating income for investors rather than capital appreciation. These funds typically invest in fixed-income securities such as bonds, preferred stocks, and other debt instruments. The main goal of income funds is to provide a steady stream of income through interest payments and dividends.

Benefits and Risks of Income Funds

Income funds offer several benefits, including:

- Regular Income: Income funds provide a reliable source of income through interest payments and dividends.

- Diversification: By investing in a variety of fixed-income securities, income funds help spread risk across different assets.

- Capital Preservation: Income funds are generally less volatile than equity funds, making them a suitable option for conservative investors looking to preserve capital.

However, there are also risks associated with income funds, such as:

- Interest Rate Risk: Income funds are sensitive to changes in interest rates, which can impact the value of fixed-income securities.

- Credit Risk: There is a risk of default by the issuers of the fixed-income securities held by income funds, leading to potential losses.

- Inflation Risk: Inflation can erode the purchasing power of the income generated by these funds over time.

Examples of Income Funds with Consistent Performance

Some income funds that have shown consistent performance over the years include:

- Vanguard High Dividend Yield Index Fund: This fund focuses on high-dividend-yield stocks, providing investors with a steady income stream.

- PIMCO Income Fund: Managed by PIMCO, this fund invests in a diversified portfolio of fixed-income securities to generate income for investors.

- Fidelity Strategic Income Fund: This fund seeks to provide a high level of current income by investing in a mix of fixed-income securities.

Index Funds

Index funds are a type of investment fund that aims to replicate the performance of a specific market index, such as the S&P 500. Unlike actively managed funds, which involve a fund manager making individual investment decisions, index funds simply aim to mirror the performance of the underlying index.

Performance Comparison

Index funds are known for their low costs and passive investment approach, which often leads to lower fees compared to actively managed funds. Studies have shown that over the long term, index funds tend to outperform actively managed funds, especially after accounting for fees and expenses.

- Index funds have consistently shown to provide competitive returns compared to actively managed funds due to their low expense ratios.

- Actively managed funds often struggle to beat their benchmark indexes over time, making index funds an attractive option for many investors.

- Index funds offer diversification across a wide range of securities, reducing individual stock risk and providing exposure to an entire market segment.

Advantages in Portfolio Diversification

Including index funds in a diversified investment portfolio can offer several advantages, such as reducing overall portfolio risk, lowering investment costs, and providing exposure to a broader market.

- Index funds provide broad market exposure, reducing the risk associated with investing in individual stocks.

- Due to their passive nature, index funds typically have lower turnover rates, resulting in lower transaction costs and taxes for investors.

- By including index funds in a diversified portfolio, investors can benefit from the overall growth of the market while minimizing risks associated with individual stock selection.

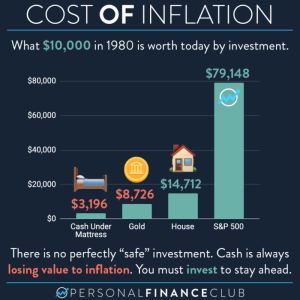

Inflation Hedge

Inflation hedge refers to investments or assets that have the potential to maintain or increase their value over time, even in the face of rising inflation rates. It is crucial in financial planning to protect the purchasing power of your money and ensure that your investments can withstand the erosive effects of inflation.

Strategies and Assets for Inflation Hedge

- Real Estate: Investing in real estate properties can serve as an inflation hedge as property values tend to rise with inflation.

- Commodities: Assets like gold, silver, and other precious metals are often considered a hedge against inflation due to their intrinsic value.

- TIPS (Treasury Inflation-Protected Securities): These government bonds provide protection against inflation by adjusting their principal value based on changes in the Consumer Price Index.

- Stocks of Inflation-Resistant Companies: Investing in companies that have pricing power and can pass on increased costs to consumers can act as a hedge against inflation.

Insurance Premiums as an Inflation Hedge

Insurance premiums can also act as a hedge against inflation over time. When you lock in a premium rate for your life insurance policy, you are essentially protecting yourself from the impact of future inflation on the cost of insurance. By paying a fixed premium amount, you ensure that your coverage remains intact regardless of how inflation affects the overall cost of living.

This can provide peace of mind and financial security for you and your loved ones in the long run.

Insurance Premiums

Insurance premiums are the amount of money an individual or business pays to an insurance company in exchange for insurance coverage. These premiums can vary depending on the type of insurance and the level of coverage desired.

Types of Insurance Premiums

- Health Insurance Premiums: These are the regular payments made to health insurance companies to maintain coverage for medical expenses.

- Auto Insurance Premiums: These are payments made to auto insurance companies to cover potential damages or losses related to a vehicle.

- Life Insurance Premiums: These are payments made to life insurance companies to provide financial protection to beneficiaries in case of the policyholder’s death.

Determination of Insurance Premiums

Insurance companies determine the cost of premiums based on several factors, including:

- The type of insurance coverage being offered

- The age, health, and lifestyle of the insured individual

- The amount of coverage being sought

- The level of risk associated with the insured individual or property

Factors Impacting Insurance Premiums

- Age: Younger individuals typically pay lower premiums as they are considered lower risk.

- Health: Individuals with pre-existing conditions may face higher premiums due to increased risk.

- Lifestyle: Risky behaviors such as smoking or extreme sports can lead to higher premiums.

- Claims History: Individuals with a history of frequent insurance claims may see higher premiums.

As we conclude our exploration of life insurance premiums for 2024, remember that informed decisions pave the way to financial security and peace of mind. Stay vigilant, stay protected.

Helpful Answers

What factors can influence life insurance premiums?

Factors such as age, health condition, occupation, and lifestyle choices can impact life insurance premiums.

How are insurance premiums calculated?

Insurance premiums are calculated based on factors like risk assessment, coverage amount, and the type of policy chosen.

What are income funds and how do they relate to life insurance premiums?

Income funds are investment vehicles that provide regular income. While not directly related to life insurance premiums, they play a role in financial planning.

Can insurance premiums act as a hedge against inflation?

Yes, insurance premiums can serve as a hedge against inflation over time, providing a measure of financial protection.