Income Funds vs Growth Funds sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with casual formal language style and brimming with originality from the outset.

As we delve into the intricacies of income funds and growth funds, we uncover the contrasting strategies and risk profiles that define these investment options.

Income Funds vs Growth Funds

Income funds and growth funds are two common types of mutual funds that cater to different investment objectives and risk profiles.Income funds primarily focus on generating regular income for investors through dividends and interest payments. These funds typically invest in stable, income-generating assets such as bonds, preferred stocks, and dividend-paying stocks. The main goal of income funds is to provide a steady stream of income to investors, making them ideal for those seeking regular payouts.On the other hand, growth funds aim to achieve capital appreciation over the long term by investing in companies with strong growth potential.

These funds usually invest in growth-oriented assets such as growth stocks, emerging markets, and sectors with high growth prospects. Growth funds tend to reinvest any earnings back into the fund to fuel further growth, making them suitable for investors looking to build wealth over time.

Investment Strategies

Income funds typically employ a conservative investment strategy by focusing on income-generating assets with lower volatility. They may also incorporate a mix of fixed-income securities to diversify the portfolio and reduce risk. In contrast, growth funds pursue a more aggressive strategy by investing in high-growth companies with the potential for substantial capital appreciation. They may concentrate on specific sectors or industries that are expected to outperform the market.

Risk Profiles

Income funds are considered less risky compared to growth funds due to their conservative investment approach and focus on stable income-generating assets. These funds are suitable for investors with a low risk tolerance or those nearing retirement who prioritize income stability. On the other hand, growth funds carry higher risk due to their exposure to volatile growth stocks and sectors.

Investors in growth funds should have a longer investment horizon and a higher risk tolerance to withstand market fluctuations and potential losses.

Income Funds

Income funds are a type of mutual fund that aims to provide a steady income stream for investors through regular dividend payments. These funds typically invest in assets that pay dividends or interest, such as bonds, dividend-paying stocks, and real estate investment trusts (REITs).

Types of Assets in Income Funds

Income funds commonly hold a variety of assets to generate returns for investors. Some of the assets typically found in income funds include:

- Government and corporate bonds

- Preferred stocks

- High dividend-paying stocks

- REITs

- Money market instruments

Income funds usually focus on securities with stable income-generating potential to provide consistent returns to investors.

Importance of Dividend Payments

Dividend payments play a crucial role in income funds as they contribute significantly to the overall returns generated for investors. Companies that pay dividends often have strong financial health and stable cash flows, making them attractive investments for income funds. By receiving regular dividend payments, investors can benefit from a steady income stream, even during periods of market volatility.

Growth Funds

Growth funds are mutual funds or exchange-traded funds (ETFs) that aim to achieve capital appreciation by investing in companies with high growth potential. These funds typically focus on investing in companies that are expected to grow at a faster rate compared to the overall market.

Investment Approach of Growth Funds

Growth funds typically follow an aggressive investment approach, seeking to invest in companies with strong growth prospects. These funds often target companies in sectors such as technology, healthcare, consumer discretionary, and other industries that are poised for rapid expansion. The fund managers of growth funds often look for companies with innovative products or services, strong earnings growth, and a competitive edge in their respective markets.

- Invest in companies with high growth potential

- Focus on sectors such as technology, healthcare, and consumer discretionary

- Seek companies with innovative products/services and strong earnings growth

Industries or Sectors Where Growth Funds Invest

Growth funds often invest in industries or sectors that are expected to experience above-average growth compared to the broader market. Some examples of industries where growth funds frequently invest include:

- Technology: Growth funds often target companies in the technology sector, including software, hardware, and internet companies.

- Healthcare: Companies in the healthcare sector, such as biotechnology and pharmaceutical companies, are popular picks for growth funds.

- Consumer Discretionary: Growth funds may invest in companies that cater to consumer spending, such as retail, leisure, and entertainment companies.

Inflation Hedge

Income funds and growth funds can both serve as a hedge against inflation by providing returns that outpace the rate of inflation over time. This is important for investors looking to preserve the purchasing power of their investments in the face of rising prices.

Income Funds as Inflation Hedge

Income funds typically invest in assets that generate regular income, such as dividend-paying stocks, bonds, and real estate investment trusts (REITs). These investments can help protect against inflation in the following ways:

- Dividend-paying stocks: Companies that consistently pay dividends tend to increase their dividend payments over time, which can provide a growing income stream that keeps pace with inflation.

- Bonds: Inflation-linked bonds, also known as TIPS (Treasury Inflation-Protected Securities), adjust their principal value in response to changes in inflation, providing investors with a hedge against rising prices.

- REITs: Real estate investments often have rental income that can increase with inflation, making them a potential hedge against rising prices.

Growth Funds as Inflation Hedge

Growth funds, on the other hand, typically invest in companies with high growth potential. While growth funds may not offer immediate income like income funds, they can still act as a hedge against inflation by focusing on companies that have the ability to grow their earnings over time. These investments can outpace inflation and provide capital appreciation that protects against the eroding effects of rising prices.Overall, income funds are generally considered a better hedge against inflation due to their focus on generating regular income that can keep up with rising prices.

However, a diversified portfolio that includes both income and growth funds can provide a more balanced approach to inflation protection.

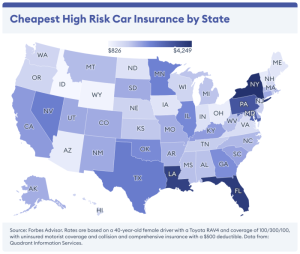

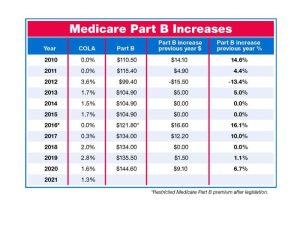

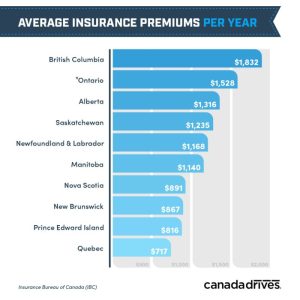

Insurance Premiums

Investing in income funds or growth funds can have an impact on insurance premiums. The relationship between these types of funds and insurance premiums is important to consider when planning your investment strategy.When it comes to insurance premiums, income funds are generally seen as a more stable option compared to growth funds. Income funds typically consist of investments in fixed-income securities like bonds, which provide a steady stream of income through interest payments.

This stable income can help offset the costs of insurance premiums, providing a reliable source of funds to cover these expenses.On the other hand, growth funds are more focused on capital appreciation and may not always provide a consistent income stream. While growth funds have the potential for higher returns, they also come with greater volatility. This can make it challenging to rely on growth funds alone to cover insurance premiums, as the fluctuating returns may not always be sufficient to meet these costs.

Strategies for Offsetting Insurance Premium Costs

One strategy for using income or growth funds to offset insurance premium costs is to create a balanced portfolio that includes both types of funds. By diversifying your investments, you can take advantage of the stability of income funds while also benefiting from the growth potential of growth funds.Another strategy is to periodically review your investment portfolio and adjust your allocations based on your insurance needs.

For example, if you anticipate an increase in insurance premiums, you may consider reallocating some of your investments from growth funds to income funds to ensure you have enough income to cover these costs.Overall, the key is to strike a balance between income and growth funds in your investment portfolio to ensure you have a reliable source of funds to cover insurance premiums while also maximizing your investment returns.

In conclusion, Income Funds vs Growth Funds sheds light on the nuances of these investment vehicles, equipping investors with the knowledge to make informed decisions in their financial journey.

Common Queries

What are the primary differences between income funds and growth funds?

Income funds prioritize regular income generation through dividends and interest, while growth funds focus on capital appreciation by investing in companies with high growth potential.

How do income funds and growth funds act as a hedge against inflation?

Income funds may provide stability during inflation with consistent dividend payments, while growth funds can offer growth potential that outpaces inflation rates.

What types of assets are commonly held in income funds?

Income funds often hold bonds, dividend-paying stocks, and interest-bearing securities to generate steady income for investors.

How do income or growth funds impact insurance premiums?

Investing in income or growth funds can potentially increase disposable income, which may help offset insurance premium costs over time.