As Inflation Hedge Strategies for Long-Term Investors takes center stage, this opening passage beckons readers with casual formal language style into a world crafted with good knowledge, ensuring a reading experience that is both absorbing and distinctly original.

In today’s dynamic financial landscape, protecting your long-term investments against the erosive effects of inflation is crucial. This guide explores strategic approaches and tools that can help investors navigate and mitigate the impact of inflation.

Income Funds

Income funds can be a valuable component of a long-term investment strategy for investors looking to hedge against inflation. These funds typically consist of a diversified portfolio of fixed-income securities, such as bonds and dividend-paying stocks, that generate regular income for investors.

Historical Examples

Income funds that have historically acted as a hedge against inflation include Treasury Inflation-Protected Securities (TIPS), Real Estate Investment Trusts (REITs), and dividend-focused equity funds. These assets have the potential to provide a steady stream of income that can help offset the negative impact of rising prices on the overall value of the investment portfolio.

- Treasury Inflation-Protected Securities (TIPS) are government bonds designed to protect investors from inflation by adjusting their principal value based on changes in the Consumer Price Index (CPI).

- Real Estate Investment Trusts (REITs) invest in income-producing real estate properties and distribute a significant portion of their income to shareholders in the form of dividends.

- Dividend-focused equity funds hold stocks of companies with a history of consistently paying dividends, offering investors a source of income regardless of market conditions.

Advantages and Disadvantages

Income funds offer several advantages for long-term investors, including:

- Steady Income: Income funds provide a regular stream of income, which can be especially beneficial for retirees or those seeking passive income.

- Diversification: These funds typically hold a mix of assets, reducing the risk associated with investing in a single security or asset class.

- Inflation Protection: Certain income funds, such as TIPS and REITs, have historically outperformed during periods of high inflation, helping investors preserve the purchasing power of their money.

However, there are also some disadvantages to consider when investing in income funds:

- Interest Rate Risk: Fixed-income securities within income funds are sensitive to changes in interest rates, which can impact the fund’s performance and income potential.

- Market Risk: Like any investment, income funds are subject to market fluctuations and economic uncertainties that can affect their value and returns.

- Tax Implications: The income generated from these funds may be subject to taxation, potentially reducing the overall returns for investors.

Index Funds

Index funds are a type of mutual fund or exchange-traded fund (ETF) that aims to track the performance of a specific market index, such as the S&P 500. These funds provide investors with a diversified portfolio that mirrors the holdings of the underlying index.

How Index Funds Hedge Against Inflation

Index funds can serve as a hedge against inflation for long-term investors due to their passive management style and low fees. As inflation rises, the prices of assets held by the index also tend to increase, leading to higher returns for investors. Additionally, the diversification offered by index funds helps spread out risk and protect against the negative impact of inflation on individual securities.

Performance Comparison with Actively Managed Funds

During periods of high inflation, index funds have historically outperformed actively managed funds. This is because actively managed funds often have higher fees and turnover, which can erode returns, especially in inflationary environments. Index funds, on the other hand, tend to have lower fees and turnover, resulting in better performance over the long term.

Tips for Selecting the Right Index Funds

When selecting index funds for a long-term investment portfolio, consider factors such as the expense ratio, tracking error, and the index being tracked. Look for funds with low expense ratios to maximize returns, and choose funds with lower tracking error to closely mirror the performance of the index. Additionally, ensure that the index being tracked aligns with your investment goals and risk tolerance.

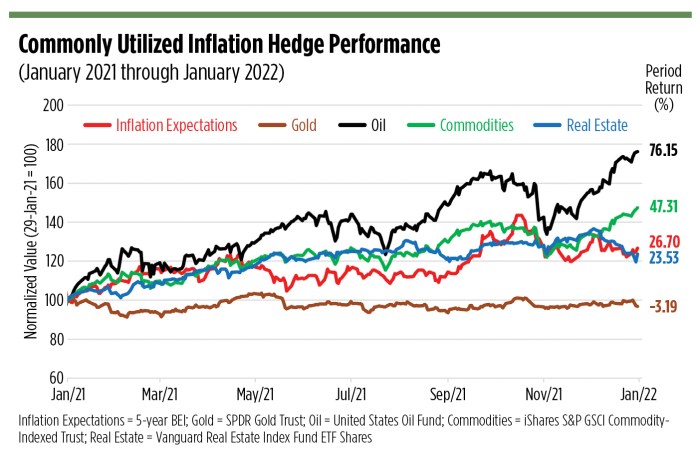

Inflation Hedge

An inflation hedge is an investment that is expected to retain or increase its value over time, even in the face of rising inflation. This is essential for long-term investors as inflation erodes the purchasing power of money, making it crucial to protect the value of their investments.

Types of Inflation Hedge Assets

- Real Estate: Properties tend to appreciate in value over time, providing a hedge against inflation.

- Commodities: Assets like gold, silver, and oil are commonly used as inflation hedges due to their intrinsic value.

- TIPS (Treasury Inflation-Protected Securities): These bonds are indexed to inflation to protect investors from the negative effects of rising prices.

- Equities: Stocks of companies with strong pricing power or those in sectors that benefit from inflation can also serve as inflation hedges.

Effectiveness of Inflation Hedge Strategies

During different economic conditions, the effectiveness of inflation hedge strategies can vary. For example, real estate may perform well during periods of high inflation as property values rise, while TIPS may be more effective during times of moderate inflation. It is important for investors to diversify their portfolio with a mix of these assets to ensure they are adequately protected against inflation.

Insurance Premiums

Inflation can impact insurance premiums for long-term investors, as the cost of insurance coverage may increase over time due to rising prices and expenses in the insurance industry. This can erode the purchasing power of an investor’s portfolio if not managed effectively.

Relationship Between Insurance Premiums and Inflation

Insurance products such as inflation-indexed annuities or inflation-protected life insurance policies can help mitigate the impact of inflation on a portfolio. These products are designed to adjust payouts or benefits based on changes in the inflation rate, providing a hedge against the erosion of purchasing power over time.

- Inflation-indexed annuities: These annuities provide payouts that are adjusted periodically based on changes in the inflation rate, ensuring that the investor’s income keeps pace with rising prices.

- Inflation-protected life insurance policies: These policies offer benefits that are adjusted for inflation, providing a higher payout to beneficiaries to account for the increased cost of living.

By incorporating insurance products that are linked to inflation, long-term investors can safeguard their portfolios against the erosive effects of inflation and ensure that their financial goals are protected.

Considerations for Incorporating Insurance Premiums in an Inflation Hedge Strategy

When incorporating insurance premiums as part of an inflation hedge strategy, investors should consider factors such as the cost of the insurance products, the level of protection provided, and the terms and conditions of the policy. It is important to carefully assess the benefits and drawbacks of each insurance product to determine its suitability for the investor’s financial goals and risk tolerance.

- Cost-effectiveness: Evaluate the costs associated with insurance premiums and compare them to the potential benefits of protection against inflation.

- Policy features: Understand the features of the insurance product, such as the adjustment mechanism for inflation, the payout structure, and any limitations or exclusions that may apply.

- Long-term impact: Consider the long-term impact of incorporating insurance premiums in an inflation hedge strategy and assess how these products can contribute to the overall diversification and risk management of the investment portfolio.

In conclusion, adopting well-thought-out inflation hedge strategies is paramount for long-term investors looking to safeguard their portfolios. By diversifying through income funds, index funds, and other inflation-hedging assets, investors can better position themselves to weather economic uncertainties and preserve the value of their investments over time.

Clarifying Questions

What are some key benefits of using income funds as part of a long-term investment strategy?

Income funds can provide steady returns through dividends and interest payments, serving as a reliable income source for investors, especially during periods of inflation.

How do index funds compare to actively managed funds in terms of hedging against inflation?

Index funds typically have lower management fees and aim to replicate the performance of a specific market index, making them cost-effective and efficient tools for inflation hedging compared to actively managed funds.

Which insurance products are commonly used to mitigate the impact of inflation on investment portfolios?

Insurance products such as inflation-protected annuities and variable universal life insurance can help investors hedge against inflation by offering protection and potential growth opportunities.